Austrian Banking Act (BWG; Bankwesengesetz)

deposit-taking business

Where capital is not collected in the form of crypto assets, but are instead collected in the form of a currency that is legal tender and the ICO foresees the repayment of such funds, then the activity requiring a licence of deposit-taking business as defined in Article 1 para. 1 no. 1 (receiving of funds from other parties for the purpose of management) or no. 2 (receiving of funds from other parties as deposits) of the Austrian Banking Act (BWG; Bankwesengesetz).

Issuing and administering means of payment

Regardless of the form in which capital is raised (whether using crypto assets or currencies that are legal tender), if the ICO stipulates that the generated Coin is intended to be deployed as a payment instrument, then depending on the specific design of the ICO, the activity requiring a licence of issuance and administration of payment instruments in accordance with Article 1 para. 1 no. 6 BWG may be fulfilled.

Third-party securities underwriting

Article 1 para. 1 no. 11 BWG contains a separate activity requiring a licence, for the participation in underwriting of third-party issues in certain instruments (e.g. transferable securities) The realisation of an issuance of a bond in the form via the blockchain (as a “tokenised” bond) for a company, i.e. the realisation of an issuance, taking over of securities/instruments as well as their placement and the associated services therewith would constitute this activity.

Custody business

Safekeeping and administration of securities on a commercial basis for other parties requires a licence in accordance with Article 1 para. 1 no. 5 BWG as custody business, regardless of the technical manner, e.g. using blockchain and smart contracts, provided that a custody agreement exists. An agreement is concluded about the tokenisation of a transferable security and smart contracts made available for saving data and managing all of the rights and obligations associated with the bonds.

Securities Supervision Act 2018 (WAG 2018; Wertpapieraufsichtsgesetz 2018)

Coins or tokens may constitute financial instruments as defined in the Securities Supervision Act 2018 (WAG 2018) in particular transferable securities. There is a strong indication for such a classification, if the rights associated with the coin or token are comparable to well-known categories of securities. In particular the granting of voting rights, shares in profits, tradability, the promise of interest payments or the repayment of the capital received at the end of a specific term therefore speak for the existence of a security (Also see the section on “security tokens”). The classification under supervisory law is conducted on a case-by-case basis and depending on the specific design.

Depending on the design of the coin or token, it may also not be possible to exclude a classification as defined in WAG 2018, even where the instrument is not a transferable security.

In such instances, depending on the advanced design of the ICO an investment service requiring a licence under the WAG 2018 may exist.

Capital Market Act (KMG; Kapitalmarktgesetz)

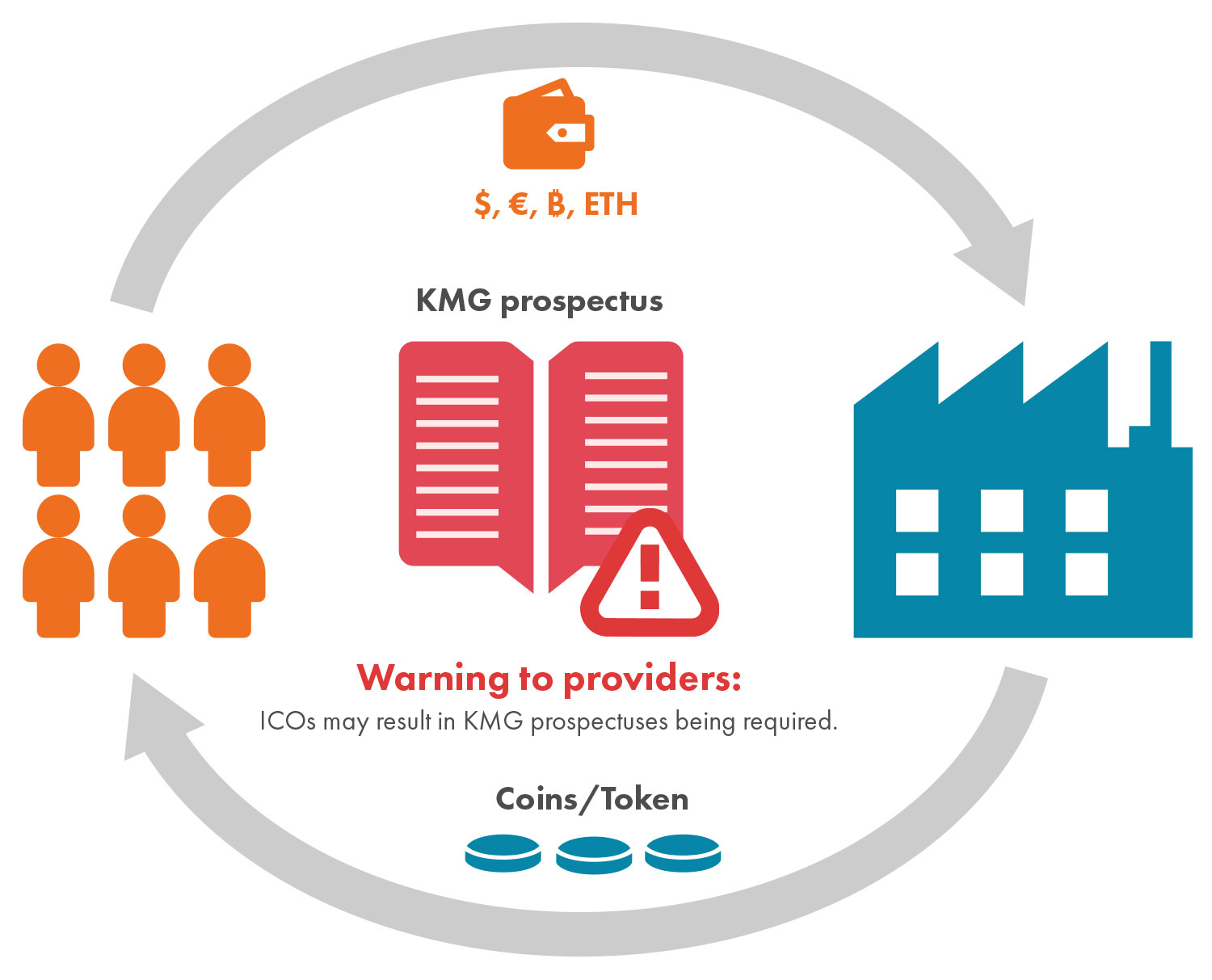

The public offering or the authorisation of access to a regulated market for securities or the public offering of investments in Austria is generally subject to the obligation to publish a prospectus in accordance with the Capital Market Act (KMG; Kapitalmarktgesetz). If as described above a transferable security as defined in the WAG 2018/KMG should exist (see also the section on “security tokens”), then accordingly a securities prospectus as defined in the Capital Market Act (KMG; Kapitalmarktgesetz) must be drawn up and published. If it is not a transferable security as defined in the KMG/WAG 2018, coins or tokens may still require a prospectus as an investment (investment prospectus). This applies for example in the case that a coin/token grants proprietary rights to the respective holder, such as rights to a claim, membership rights or conditional rights (e.g. ownership rights, claims to dividends or repayment) against the ICO organiser, and the investors collectively or together with the issuer form a risk-sharing group, but where a transfer is not possible or is only possible with some difficult.

E-Money Act 2010 (E-Geldgesetz 2010) and the Payment Services Act 2018 (ZaDiG 2018; Zahlungsdienstegesetz 2018)

When conducting an ICO in addition to the requirements set out in the Austrian Banking Act (BWG; Bankwesengesetz) the financial market supervision rules of the E-Money Act 2010 (E-GeldG 2010; E-Geldgesetz 2010) as well as the Payment Services Act 2018 (ZaDiG 2018; Zahlungsdienstegesetz 2018) may also be fulfilled.

What is electronic money?

Electronic money is defined in Article 1 para. 1 E-GeldG 2010 as all electronically stored, including magnetically stored, monetary value in the form of a claim on the electronic money issuer, issued on receipt of funds for the purpose of making payment transactions as defined in Article 4 no. 5 of the Payment Services Act 2018 (ZaDiG 2018; Zahlungsdienstegesetz 2018), and which is accepted by a natural or legal person other than the electronic money issuer.

Which coins or tokens are covered by the E-Money Act 2010?

From the outset in functional terms payment tokens as electronic money come into consideration, which with payment transactions are intended to be conducted and which should be accepted by third party acceptors as means of payment.

In contrast to other crypto assets (such as Bitcoin) in the case of ICOs there is generally a “central issuing body”, thereby satisfying the requirement of an issuer. In order to correspond to the requirements of Article 1 para. 1 E-GeldG 2010, the issuance (of the “token”) must furthermore take place against the payment of an amount of money. For this purpose legal means of payment come into consideration, whether in the form of cash or a scriptural currency. Payments are made in domestic currencies as well as in foreign currencies, and also those from third countries. Moreover, a proprietary right must exist against the electronic money issuer.

Whether an ICO is captured by the obligation for approval set out in the E-GeldG 2010 depends primarily upon its specific design (case-by-case review) and whether in this context it results in a payment of “money” (legal means of payment).

Provision of Payment Services

The provision of payment services on a commercial basis generally also requires a corresponding licence to be held. In the case of an ICO the requirements for the issuance of payment instruments or the acquiring of payment transaction might be fulfilled (Article 1 para. 2 no. 5 ZaDiG 2018).

What is a payment instrument?

A payment instrument is any personalised device and/or personalised set of procedures agreed between the payment service user and the payment service provider and used in order to initiate a payment order (Article 4 no. 14 ZaDiG 2018).

Typical payment instruments include online banking with a PIN or the use of a debit card with a PIN.

Which coins or tokens are covered by the Payment Services Act 2018?

In principle any instrument can be considered as a payment instrument that is used to make a payment order, and therefore the term is to be understood in very broad terms. Ultimately in the case of an ICO it depends whether the issued token is personalised, or whether it is designed in such a way the it may be used by every holder and therefore is transferable (reviewed on a case-by-case basis).

Moreover the application of the ZaDiG 2018, as also already is the case in the E-GeldG 2010, generally excludes when money (legal instruments of payment) is not transferred.

Alternative Investment Fund Managers Act (AIFMG)

Furthermore, an ICO may also fall within the scope of application of the Alternative Investment Fund Managers Act (AIFMG; Alternative Investmentfonds Manager-Gesetz). Where capital is collected from a majority of the investors, in order to invest it in accordance with a defined investment strategy for the benefit of the holder of the token/coin, then an alternative investment fund (AIF) exists, and the administrator of this AIF (as a rule the issuer in the case of an ICO) is in this case to observe the rules set out in the AIFMG.